“I was worried this was the beginning of the end” - UK bond market nearly collapses, BoE steps in to save it

All that Gilters is not sold.

Turmoil rocked British credit markets on Wednesday in the clearest sign yet that many corners of the financial system are ill-prepared for a high inflation, high rate regime. UK Pension funds, which collectively control over £1.5 trillion ($1.65 trillion), were forced to dump UK government bonds to stump up cash for margin calls on levered positions. The market for Gilts, as UK government bonds are known, was restored to order only by emergency action from the Bank of England, the UK’s central bank. A London-based banker, speaking to the Financial Times, said that he “was worried this was the beginning of the end. It was not quite a Lehman moment. But it got close.”

Pension funds, which are meant to be sleepy buy-and-hold investors focused on the long-term, seem like an odd source of market turbulence. In an ideal world, pension funds could simply purchase bonds appropriate for their cash-flow needs and hold them until maturity. But it is a quirk of accounting that forces pension funds to use leverage, with its decidedly short-term concern of margin calls. To stylize the matter, suppose that a pension fund will have to pay out £1 million in ten years. To match this liability, the fund purchases two £500,000 face value zero-coupon ten-year bonds, one paying out at 2.5%, and a riskier one paying out at 5%.

Today, the 2.5% bond will be valued at about £390,600, and the 5% bond will be valued at about £307,000. The pending liability, however, is still a flat £1 million, leaving the fund with a £302,400 hole in its balance sheet. While this deficit only exists on paper, it is embarrassing for the pension fund managers, who have to explain to regulators and pensioners why the fund appears insolvent. To mitigate this, accounting rules allow the fund to carry the liability on its books at present value as well. Using a hypothetical rate of 3%, the upcoming payout is worth about £744,100. While this still values the payout higher than the bonds, discounting the payout moderates the deficit, which shrinks to £46,500.

If interest rates decline, though, this scheme begins to fall apart. Suppose the three interest rates each fall by a full percentage point. This will cause the balance sheet deficit to grow to about £51,700. As interest rates continue to fall, the insolvency of the fund (on paper) continues to grow. Since the payout is carried on the books at a higher initial value than the bonds, liabilities will grow faster than assets for the same interest rate decline. One clever way around this issue is to lever the assets. By borrowing money to purchase more bonds, the book value of assets can be juiced to match liabilities, equalizing the impact of rate changes across both sides of the balance sheet.

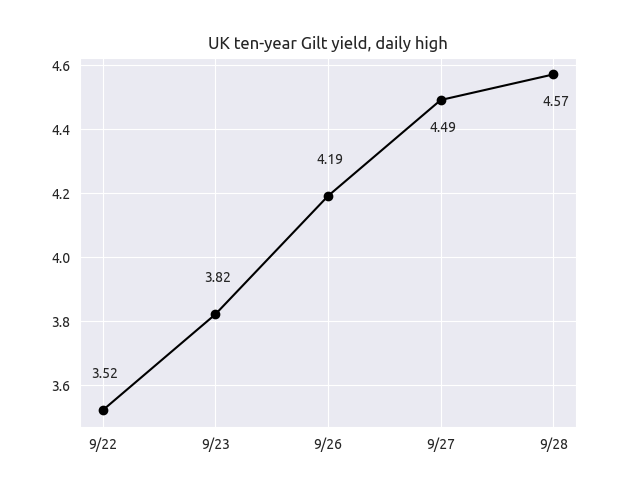

Of course, buying assets on margin exposes investors to new risks, a fact that pension funds rudely discovered on Wednesday. This week, Kwasi Kwarteng, the British chancellor, unveiled an unpopular and irresponsible fiscal plan that roiled British investors. In anticipation of new bond issuance to fund the plan, yields on Gilts spiked, with the ten-year reaching 4.19% on Monday. Prices, which move inversely to yields, collapsed. Pension funds, holding levered bets on Gilts, faced calls for more collateral from their lenders. To quickly meet these margin calls, pension funds unloaded the most liquid asset they could: Gilts.

The Gilt fire sale only served to drive prices down further, spurring further margin calls. According to some market participants, the market for Gilts went ‘no bid’, meaning there was not a single buyer for UK government debt. As the value of the Gilts on the books of pension funds continued to be marked down, some faced serious risk of insolvency, prompting the Bank of England to step in and provide market liquidity. Starting Wednesday, the Bank promised to purchase up to £5 billion of long-dated gilts per day to restore stability. The move drew support from those fearing the UK bond market would break, and criticism from those who saw the Bank’s purchases as incompatible with monetary tightening.

The Bank’s support was ultimately necessary to keep the vital government bond market functioning, even if it looked strikingly at odds with most central bank behavior this year. Quantitative tightening is a regime shift that will take years to unfold, and there is nothing incongruous about needing to act as a liquidity provider for sound assets during brief market flare ups. In many ways, the Bank of England was engaged in a refreshingly classic mission of central banking, in a time when unconventional monetary policy tools have become part of the standard kit. But if the newly formed UK government does not take this crisis as a wake up call to reform their fiscal policy, the Bank of England may find themselves with many more fires to extinguish.