Tether's Balance Sheet Operations

Funding quasi-dollars with dollars can make things weird.

Years ago, if you had asked me which crypto institution was most likely to lead to a market collapse, I would have said Tether. The company’s stablecoin USDT is vital to the crypto ecosystem, with a $123 billion market cap and a daily volume that dwarfs competitors like USDC. But for the amount of money riding on its continued success, Tether is an extraordinarily sketchy enterprise.

While the company has become more professional over the years, they have long refused a formal audit or a detailed accounting of what comprises their reserves. In fact, an investigation by the New York State Attorney General’s office determined that Tether lied about the status of reserves backing USDT and operated for months in 2017 without access to the banking system.

While I’m still highly skeptical about Tether, USDT’s longevity is undeniable at this point. The token has maintained its $1 peg for about a decade, deviating in only a few short-lived episodes. My interest in Tether was renewed by my recent reading of Zeke Faux’s excellent book Number Go Up, which I strongly recommend for more background on the company and a critical look at the collapse of FTX.

Today, I want to sketch out my understanding of Tether’s various balance sheet operations. While this might seem like an exercise in taxonomy, looking at these mechanics offers some interesting insight into how Tether’s operations might influence crypto prices more broadly.

A brief intro to Tether’s balance sheet

Note: I’m only going to discuss USDT today, although Tether does have stablecoins based on other currencies too.

Tether’s activities are sometimes viewed as analogous to those of a bank, but I think that’s a bit too generous. Most banks fund themselves with a mix of flighty, short-term liabilities (like deposits) and more stable, long-term ones (like bonds). About 60% of Citigroup’s total liabilities, for instance, are deposits.

But this isn’t the case for Tether, whose liabilities solely comprise USDT. Per Tether, USDT has no lock-up period and can (supposedly) be exchanged on demand for real dollars sent to a bank account (with a minimum amount of $100K). Therefore, Tether is more like a money market fund, as both operate solely with short-term liabilities.

Starting from scratch, when the first individual wired Tether actual dollars in exchange for USDT, here’s a basic schematic of what the company’s balance sheet looked like:

Now that Tether has these dollars, however, they might want to earn a bit more yield than what a bank account can offer. After all, since Tether doesn’t pass on interest to USDT holders, any yield generated is pure profit for the company.

Tether’s most basic and least controversial practice is to swap a portion of these deposits for another safe asset like US Treasuries (or traditional money market funds, secured repos, etc.). Since any of these options are basically as good as cash, we can lump them all together as Tether’s first balance sheet operation: buying cash-like instruments with dollars.

There are some mark-to-market risks here on the Treasuries if interest rates rise, especially since we’re not giving Tether a capital cushion. Still, this is a fairly safe way for Tether to generate profit without taking significant solvency risks. So far, so good.

Lending dollars to private borrowers

Okay, we now have Tether earning a yield on Treasuries. But lending to the US government is extremely safe - why not take on some extra risk to juice up returns?

This leads us to Tether’s second balance sheet operation: lending to private borrowers. This is generally more controversial than the first operation, but the exact level of risk here depends on the borrower and the terms. Lending dollars to large companies through short-term investment-grade commercial paper, for instance, is standard practice for many traditional money market funds.

Of course, some counterparties may not be so safe. At one point, Tether was purchasing vast quantities of commercial paper from Chinese issuers of questionable quality, for instance.

Buying speculative assets with dollars

We’ve now climbed the ladder of credit quality from Treasuries to corporate borrowers, but why limit ourselves to fixed-income investments? Tether’s current attestations show holdings of precious metals, so let’s add some gold to the mix.

This is Tether’s third balance sheet operation: buying speculative investment assets with dollars. (You might quibble that gold shouldn’t really be considered a speculative investment asset, but the metal’s price is far more volatile than many people think.)

It should go without saying, but adding speculative assets like this to the balance sheet raises the risk profile substantially. The value of investment assets can fluctuate a lot, meaning insolvency is a much greater risk without a strong capital cushion. This is why traditional money market funds are basically barred from holding anything other than short-term high-quality fixed-income instruments.

One point worth noting here is that Tether could use their dollars to buy speculative crypto assets as well (for instance, by depositing dollars at an exchange and using them to buy Bitcoin). Later on, though, I’ll describe a much more interesting way for Tether to buy crypto assets.

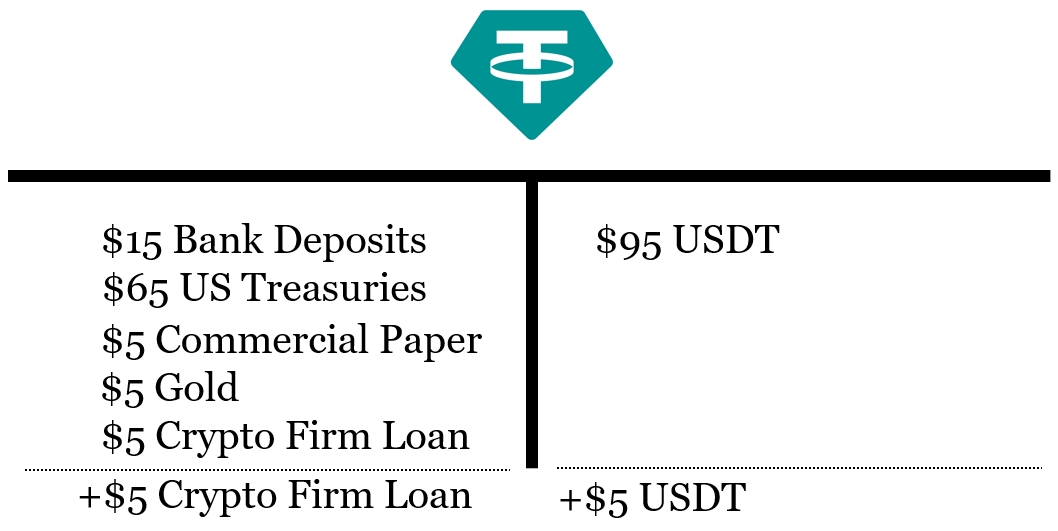

Lending USDT to private borrowers

Here’s where things get tricky. So far, we’ve been manipulating the left-hand side of the balance sheet, adjusting the composition of Tether’s dollar assets. But just like a bank can create bank deposits out of thin air, so too can Tether create USDT from nothing.

While these tokens can’t be lent out as widely as Tether’s dollars can, there are plenty of crypto firms who would happily borrow USDT to make their own bets. Perhaps there are even individuals who would prefer an untraceable USDT loan over traditional dollar financing through a bank. Thus, lending out USDT is Tether’s fourth balance sheet operation.

For what it’s worth, Tether claims to only issue new tokens when they are “requested and purchased by customers.” But considering that Tether does in fact lend out USDT (including in its infamous loan to Celsius), this can’t possibly be true unless the firm was employing an improbable and convoluted buyback/relending program.

Let’s note a few things here:

This operation increases the size of Tether’s balance sheet without new customers exchanging dollars for USDT. In the intro to this article, I used the size of Tether’s USDT issuance as a scale for the token’s customer adoption - but that’s misguided if Tether is also simply printing USDT.

It is incorrect to state that Tether is ‘loaning out customer funds’ if those loans are made in USDT.

But regardless of point 2, this type of lending is still risky for customers. Once the crypto firm has spent its borrowed USDT, the tokens are out in the marketplace and can be brought to Tether for redemption by their new holders, at which point the company may or may not be liquid or solvent enough to honor that request.

One way to help navigate point 3 is to demand collateral from crypto firms, likely in the form of Bitcoin or another ‘reliable’ crypto asset. In fact, Tether does state that their USDT loans (dubbed “secured loans” in their reserves) are fully collateralized.

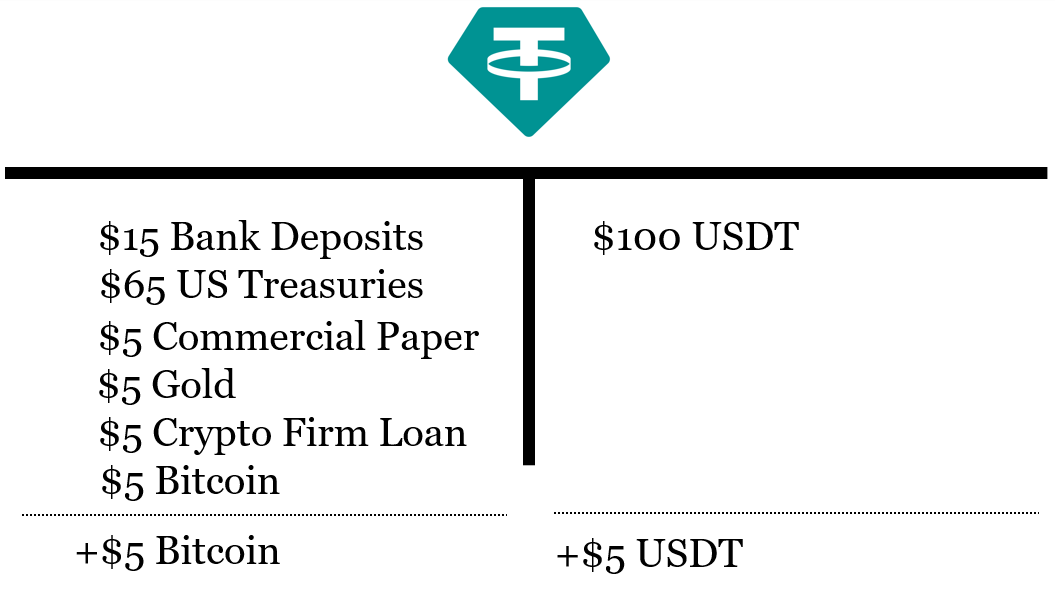

Buying crypto assets with USDT

In balance sheet operations one through three, we saw how Tether could climb the risk ladder when deploying their dollars. But they can also do the same when deploying USDT. Rather than print new USDT to lend out to crypto firms, Tether can also print new USDT to purchase crypto assets directly - their fifth balance sheet operation.

Earlier, I mentioned how Tether could buy Bitcoin with dollars through an exchange. Since stablecoins are the dollars of much of the crypto ecosystem, however, you can also buy Bitcoin with USDT directly.

In fact, the composition of assets we’ve now created is roughly similar to the makeup of Tether’s reserves as of their most recent attestation.

You might think that purchasing speculative assets with newly printed USDT is far too risky an activity for a stablecoin to engage in. At least crypto loans in USDT can be overcollateralized to offer some degree of security, for instance.

But there’s a fascinating embedded optionality here:

Imagine that Bitcoin prices go up…

Then suppose that Tether sells their Bitcoins for USDT tokens, which are held in Tether’s treasury. Since Tether is retiring more USDT than they initially printed, this results in an equity gain through a net reduction in outstanding liabilities.

Alternatively, suppose that Tether sells their Bitcoins for actual dollars. This results in an equivalent equity gain through an increase in assets. Intriguingly, this provides Tether a way to ‘cycle’ (launder?) USDT printing into actual dollars.

Imagine that Bitcoin prices go down…

Then Tether can just keep printing USDT to buy Bitcoins until that demand drives prices higher.

Eventually, Bitcoin’s rising price should draw momentum traders or speculators with FOMO into the market, providing liquidity for Tether to sell into.

See 1.

Conclusion

There are plenty of questions here that I don’t have answers to, including:

Does Tether print USDT to buy crypto assets, or does it only buy crypto assets with dollars?

If Tether does print USDT to buy crypto assets, to what extent does this activity drive prices in Bitcoin and other tokens?

How reliable are Tether’s attestations when it comes to understanding their engagement with the various balance sheet mechanisms we’ve explored? As point-in-time measurements, does Tether management window dress their reserves before attestations are conducted?

Finally, I’d just like to stress how silly engaging in any of this balance sheet nonsense is for Tether’s management.

Ignoring things like Bitcoin, crypto loans, and so-called “other investments,” Tether has something like $110 billion in actual dollar assets according to their latest attestation. Stick that in Treasury bills earning 5% and (since Tether doesn’t need to pay interest to tokenholders) the company would be among the most profitable banks in the United States - all for basically zero risk or headache.

Why even bother doing anything else?

Comments? Critiques? Questions? Reply to this email and let me know, I read everything.